What happens to a mortgage after death? Many people assume it disappears when a homeowner passes away. In reality, the mortgage typically remains attached to the property, leaving heirs with important decisions to make.

Ownership of a home can pass to family members. But the loan that goes with it usually stays in place. If you’re new to home financing, understanding what a mortgage is can help explain why the loan remains attached to the property.

This often leads to important questions:

- Can family members keep the home?

- Does the loan need to be paid off right away?

- Can heirs take over the existing mortgage?

- What protections exist under federal law?

Understanding these rules can help families make more informed decisions during a difficult time.

What Happens to a Mortgage After Death?

When a homeowner passes away, the mortgage usually remains attached to the property.

A mortgage is a secured loan tied to the home itself. The outstanding balance does not automatically disappear when the borrower dies. In many cases, heirs inherit a home along with the responsibility of deciding how the mortgage will be handled.

This means decisions must be made about:

- Keeping the home

- Refinancing the loan

- Assuming the mortgage

- Selling the property

The right choice often depends on the family’s financial situation, future plans, and the terms of the existing loan.

Understanding the Due-on-Sale Clause

Most mortgage agreements include a due-on-sale clause.

This clause gives a lender the right to demand full repayment of the loan balance when ownership of the property transfers to another person.

Example:

- Home value: $500,000

- Remaining mortgage balance: $250,000

If ownership transfers, the lender may have the right to require repayment of that $250,000 balance.

The purpose of this clause is to protect lenders when ownership changes hands.

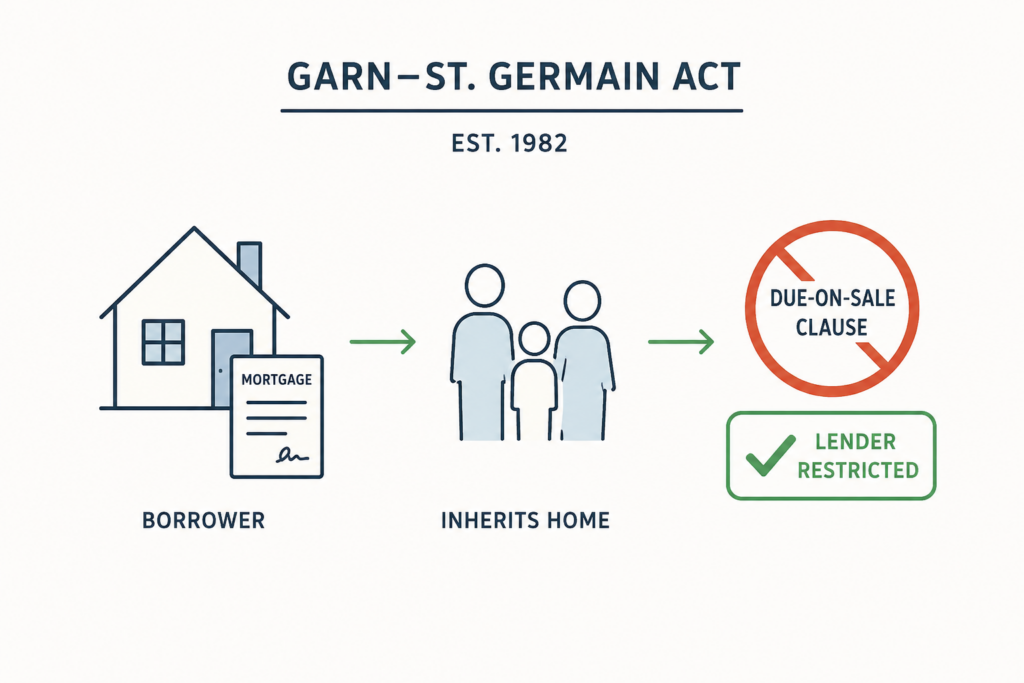

The Federal Protection Many Families Do Not Know About

Here is where things get more nuanced.

The Garn-St. Germain Depository Institutions Act of 1982 created important exceptions to the due-on-sale rule.

One key protection applies to certain family-related transfers, including inherited property.

In many cases, lenders cannot automatically enforce a due-on-sale clause simply because a property passes to an heir after a homeowner’s death. This protection is designed to help prevent unnecessary hardship for surviving family members.

Can Heirs Keep an Inherited Home?

In many situations, yes.

Federal law generally allows certain heirs and family members to inherit ownership of a property without triggering immediate repayment of the mortgage.

Common situations may include:

Property Transferred Through a Will

Ownership passes according to the homeowner’s estate plan.

Property Held in a Trust

A trust may simplify property transfer and estate administration.

Surviving Spouse Situations

Additional protections may apply depending on ownership structure and state law.

While ownership can transfer, mortgage payments generally must continue.

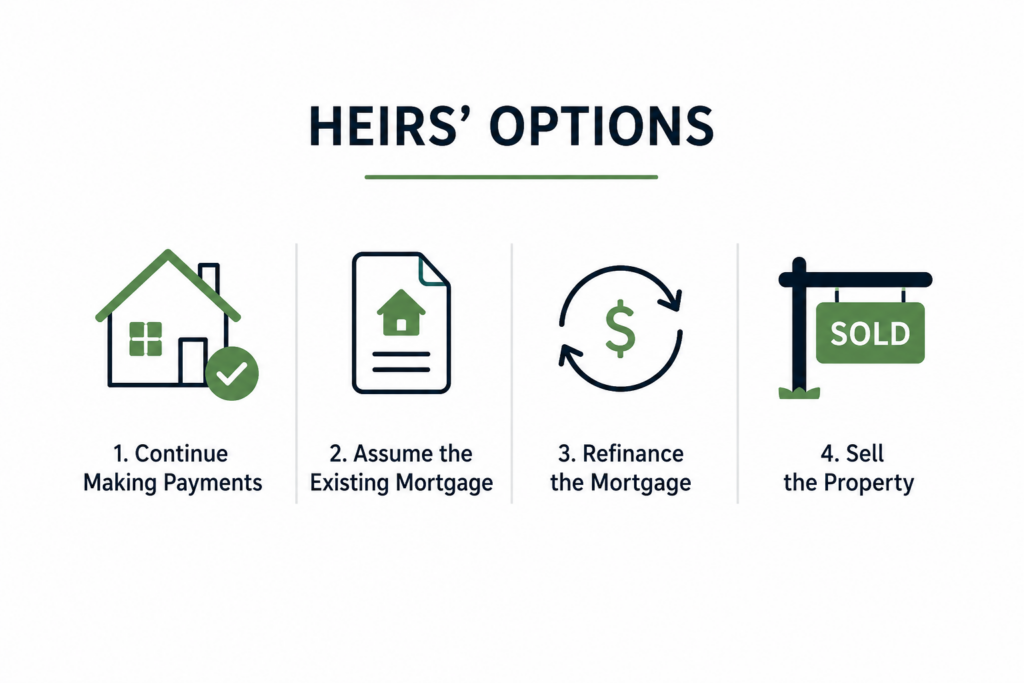

What Options Are Available to Heirs?

There is rarely a one-size-fits-all answer when inheriting a home. Several options may be available, depending on financial circumstances, long-term goals, and the remaining loan terms.

Option 1: Continue Making Mortgage Payments

Some heirs choose to keep the home and continue making payments.

Potential benefits may include:

- Preserving a family property

- Maintaining housing stability

- Keeping existing loan terms

As long as payments stay current, the loan may continue in good standing.

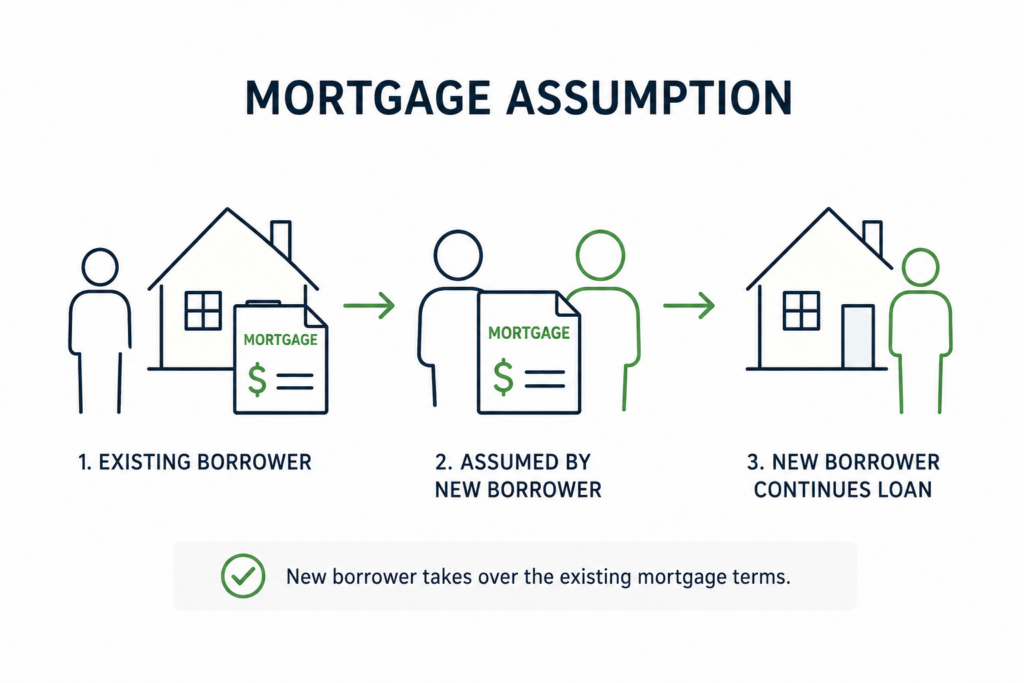

Option 2: Assume the Existing Mortgage

In some situations, heirs may be able to assume responsibility for the mortgage.

Mortgage assumption allows an eligible person to continue with the existing loan rather than replacing it with a new one.

Why this may matter:

- Mortgage originated in 2021 at 3%

- New mortgage originated today at 6% or higher

Keeping a lower interest rate could result in meaningful savings over time.

Requirements vary by lender and loan type.

Option 3: Refinance the Mortgage

Some heirs may choose to refinance. This may make sense when:

- Multiple heirs are involved

- Ownership changes are needed

- Financial restructuring is desired

Refinancing replaces the existing mortgage with a new loan.

Potential benefits:

- Updated loan terms

- Ownership adjustments

- Access to different mortgage products

Potential drawbacks:

- Higher interest rates

- Closing costs

- Qualification requirements

Option 4: Sell the Property

Selling the inherited home is another common path.

Example:

- Home value: $600,000

- Mortgage balance: $250,000

Upon sale, the mortgage is paid off. Any remaining equity may pass to the estate or the heirs.

Selling may be a good fit when:

- Heirs do not plan to live in the home

- Maintenance costs are a burden

- The property no longer fits the family’s goals

What Is Mortgage Assumption?

Mortgage assumption happens when an eligible person takes over responsibility for an existing mortgage.

Rather than paying off the current loan and starting a new one, the heir continues under the existing loan structure.

Potential advantages include:

- Keeping a lower interest rate

- Avoiding certain refinancing costs

- Maintaining familiar loan terms

Documentation and lender approval may still be required.

What Happens If Mortgage Payments Stop?

Even when ownership protections apply, mortgage obligations generally remain.

If payments are not made:

- Delinquency may occur

- Default may follow

- Foreclosure proceedings may eventually begin

It is important for heirs to contact the mortgage servicer as early as possible. Heirs may also review mortgage servicing guidance from the Consumer Financial Protection Bureau (CFPB) to better understand their rights and responsibilities.

Steps to Take After Inheriting a Home

Taking the right steps early can help reduce confusion and avoid delays. These steps may help families navigate an inherited property:

- Determine the remaining mortgage balance. Understand exactly how much is owed.

- Contact the loan servicer. Ask about available options and what documentation is needed.

- Review estate documents. Confirm ownership rights and transfer arrangements.

- Evaluate your options. Consider whether it makes more sense to keep the property, assume the mortgage, refinance, or sell.

- Seek professional guidance. Legal, tax, and mortgage professionals can provide advice tailored to your situation.

The Bottom Line

A homeowner may pass away. The mortgage usually does not.

Federal protections, such as the Garn-St. Germain Act, help many heirs avoid immediate loan acceleration under a due-on-sale clause.

Whether the best path forward involves keeping the home, assuming the mortgage, refinancing, or selling, knowing the available options can make a real difference for families navigating a mortgage after death.

Disclaimer

This article is provided for educational purposes only and should not be considered legal, tax, financial, or mortgage advice. Individual situations may vary. Readers should consult qualified legal, tax, and mortgage professionals regarding their specific circumstances.

Wonder Rates, Inc., NMLS# 1518655, DRE# 02047445, DFPI# 60DBO-59134 | Equal Housing Opportunity. Equal Housing Lender.

Leave a Reply